Vest Exchange: All You Need To Know

A high-level overview of the new and innovative approach to decentralized perpetual futures

Executive Summary

Current perp DEXs fail to properly account for risk, resulting in expensive trading fees, suboptimal returns for LPs, a lack of assets offered, lower capital efficiency, and a higher risk of insolvency

Vest addresses this issue with two core innovations:

Dynamically adjusting trading fees based on the amount of risk a trader creates

Creating two separate sources of liquidity to protect LP capital and maximize risk-adjusted returns

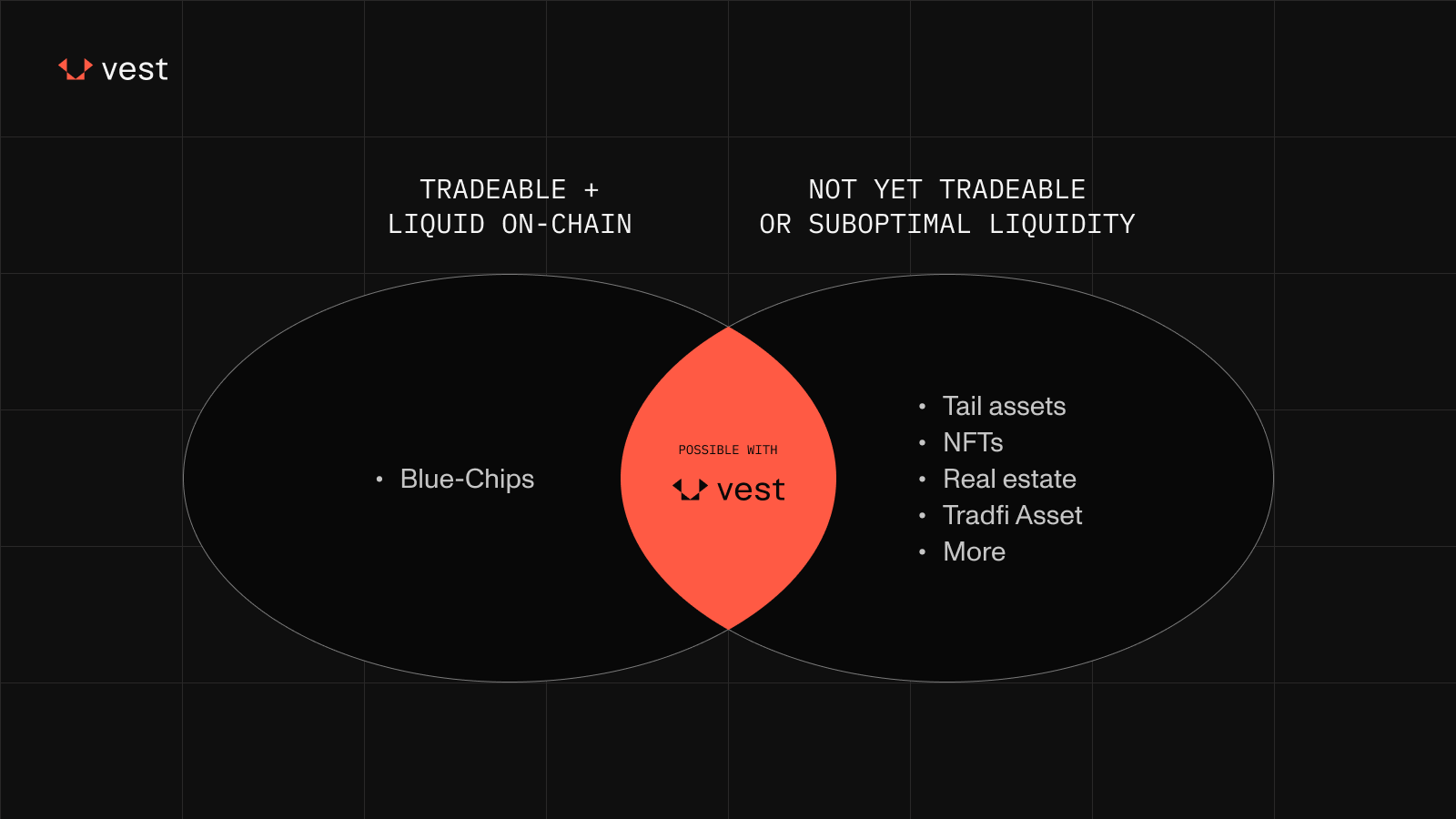

This allows Vest to easily list new assets, safely scale OI past TVL, and eventually serve as core infrastructure for a capital-efficient DeFi ecosystem with powerful cross-margining capabilities.

Background

The Vest Labs research team created Vest Exchange after years of rigorous research and discourse in the decentralized perpetual futures space. The team recognized a need for proper risk management and trade pricing, leading to traders paying too much on a per-trade basis and LPs taking on far too much risk to generate outsized returns while not being fairly compensated for that risk. The result of these efforts is a math-driven approach to mitigating risk within a system, allowing for a low cost of trading and fair returns for LPs. This risk engine, known as zkRisk, will first be applied to create a perpetual futures exchange due to their established product-market-fit on-chain.

zkRisk

Vest's risk engine defines a monetary risk measure for any given trade to calculate the capital needed to ensure solvency. A premium known as Premia is established using this risk measure by calculating the difference in capital needed before and after that trade to ensure protocol solvency. Vest conducts this computation off-chain and submits a ZK proof to an on-chain verifier, only accepting the associated transaction if the proof is correct. Premia allows Vest to take on higher-risk positions and assets without exposing LPs or the AMM to disproportionate risk.

Vest uses zkRisk to offer a perpetual futures platform where LPs provide capital that traders use to open positions, paying for the risk they create. Through this, Vest can offer trading for any asset with a price feed, safely scale OI past TVL, and offer outsized risk-adjusted returns for LPs.

Traders

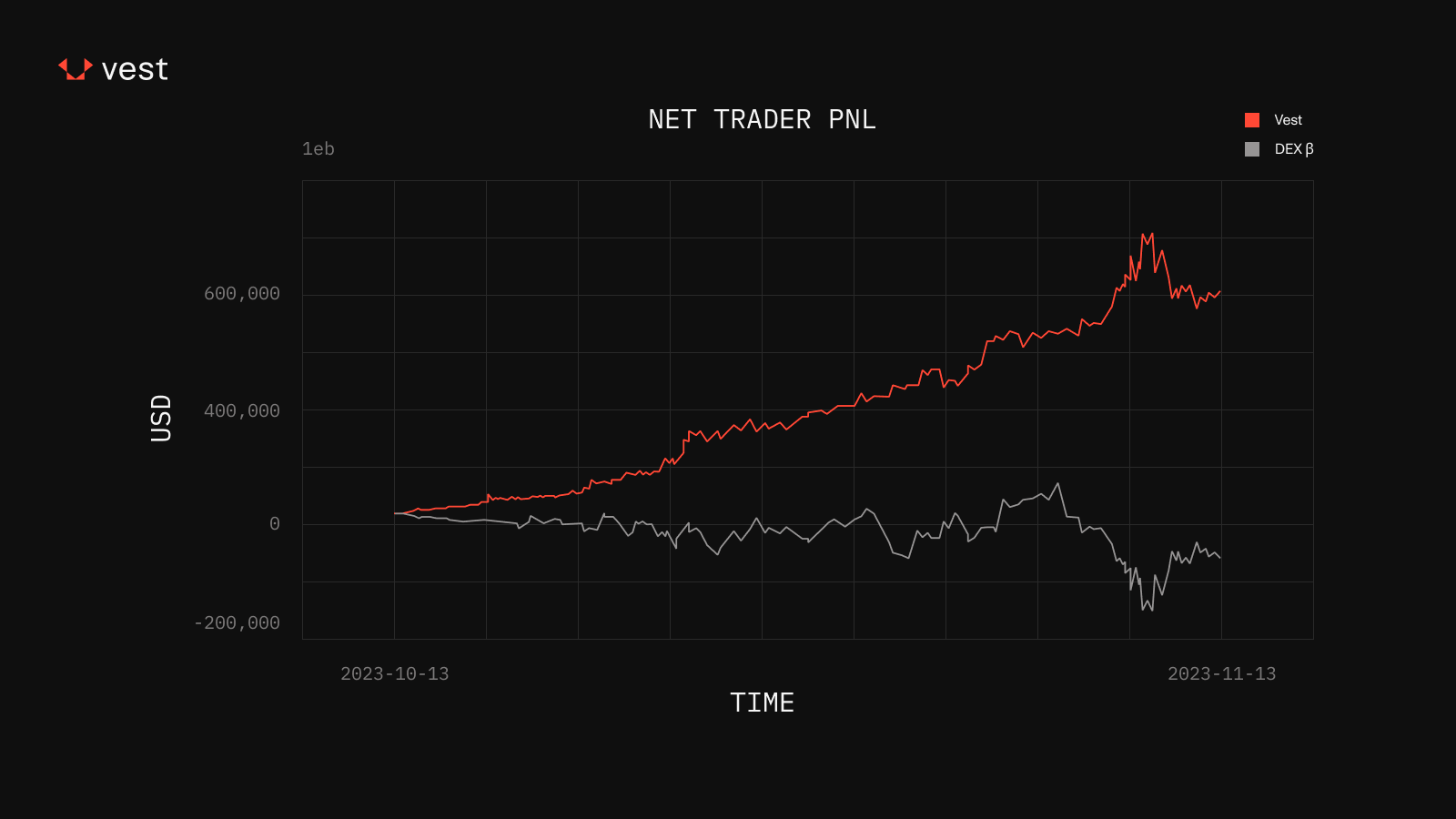

Traders pay two fees to trade on Vest, Premia and a flat execution fee. Early simulations show Vest traders paying orders of magnitude lower fees on average than their counterparts trading on fixed-fee perp dexes. This built-in risk management also allows Vest to list new assets without any drastic changes. Trader/wins and losses, regardless of asset listing, are priced in using zkRisk, preventing LPs from taking on significant losses.

As OI skew increases in any one direction for a given market, funding rate and Premia ensure that traders who exacerbate that skew compensate LPs adequately. The same risk measure used to calculate Premia is used to calculate funding rate. The same value is also split across each market via Euler Allocation to define an overall funding rate per asset. This funding rate is then split across all traders with an open position against that asset, ensuring that any change in risk is accounted for.

Liquidity Providers

Vest compensates passive LPs properly for the capital they provide via the fees traders pay and funding rate to compensate for change in risk. Premia is paid to the Vest AMM and LPs, while the flat execution fee is paid to LPs and the Vest team. Vest's AMM serves as a buffer between traders and LPs by first taking on trader profits and losses. The AMM allows LPs to generate consistent yield from both fees without having their gains wiped out by a profitable trading environment. The principal provided by LPs is intended to be fully protected and have none of its gains subsidized by trader losses. The execution fees create a predictable yield for LPs, while Premia allows them to accrue more or less yield when traders create a particularly skewed or balanced environment.

Many LP-based dexes face issues of LP profitability, generating strong and marketable yield over months only to have it wiped out and more by a single day of profitable trading. Vest's AMM buffer and risk-indifferent approach prevent these days from adversely affecting LPs while maintaining consistent yield generation.

Possibilities

Vest's on-chain perpetual futures exchange aims to be one of the most flexible and liquid on the market. In the long run, Vest will apply the zkRisk to monitor risk for an entire DeFi ecosystem, offering advanced capital-efficient DeFi Products. This ecosystem will have cross margin available across different products, allowing for fun possibilities like loans collateralized by perp positions, perp/options collateral being lent out to borrowers to generate yield, active limit orders being composable across other products, and more.

Vest's perpetual future exchange is the first and paramount step in that process. With the first product going live in the next few weeks, traders, LPs, and DeFi enthusiasts will be able to see just how impactful proper risk pricing can be for any DeFi product. Until then, any and all things related to Vest are open for academic discussion with other like-minded users on our research forum. Any updates, news, and additional info on Vest can be found first on our X and Discord, with a special opportunity to get involved today available on Discord.